Basic Health Program Workgroup

- Presentation also available in Portable Document Format (PDF)

July 31, 2013

One Commerce Plaza Albany, New York

Office of Health Insurance Programs Department of Health

Agenda

- Introductions

- Workgroup Charge

- BHP Overview

- Informing New York´s Decision on a BHP

- Impact on NYS – Studies to Date

- Open Discussion

- Next Steps

BHP Workgroup Charge

- 2013–14 Enacted Budget established the BHP Workgroup:

- §16–a. (a) The Commissioner of Health shall convene a workgroup to consider issues pertaining to the federal option to establish a basic health program for individuals who are not eligible for medical assistance under title eleven of article five of the social services law.

(b) The workgroup shall: evaluate federal guidance related to basic health programs; discuss fiscal, consumer, and health care impacts of a basic health program; and consider benefit package, premium and cost–sharing options for a basic health program.

- §16–a. (a) The Commissioner of Health shall convene a workgroup to consider issues pertaining to the federal option to establish a basic health program for individuals who are not eligible for medical assistance under title eleven of article five of the social services law.

BHP Workgroup Membership

- Chair:

- Judith Arnold, Division of Health Reform and Exchange Integration

- Members:

- Elisabeth Benjamin, Community Services Society

- Kate Breslin, SCAA

- Lauri Cole, NYS Council for Community Behavioral Healthcare

- Jeffery Gold, HANYS

- Assemblyman Richard N. Gottfried, Assembly Majority

- Senator Kemp Hannon, Senate Majority

- Trilby de Jung, Empire Justice Center

- Joseph Maldonado, Jr., MSSNY

- Bertram Scott, Affinity Health Plan

- Kathy Shure, GNYHA

- Richard Winsten, Meyer Suozzi English and Klein

- Robert Wychulis, AMERIGROUP NY, LLC

- Paul Zurlo , EmblemHealth

BHP Overview

- ACA gives states the option to establish a Basic Health Program for:

- Individuals with incomes between 138–200% FPL who are ineligible for Medicaid or CHIP, and do not have access to affordable employer coverage.

- Individuals with incomes below 138% of FPL who are ineligible for Medicaid due to immigration status.

- Federal government gives states 95% of what would have been spent on APTC in the marketplace.

- Health plans must include essential health benefits.

- Monthly premiums and cost sharing cannot exceed the amount the individual would have paid for coverage in the marketplace.

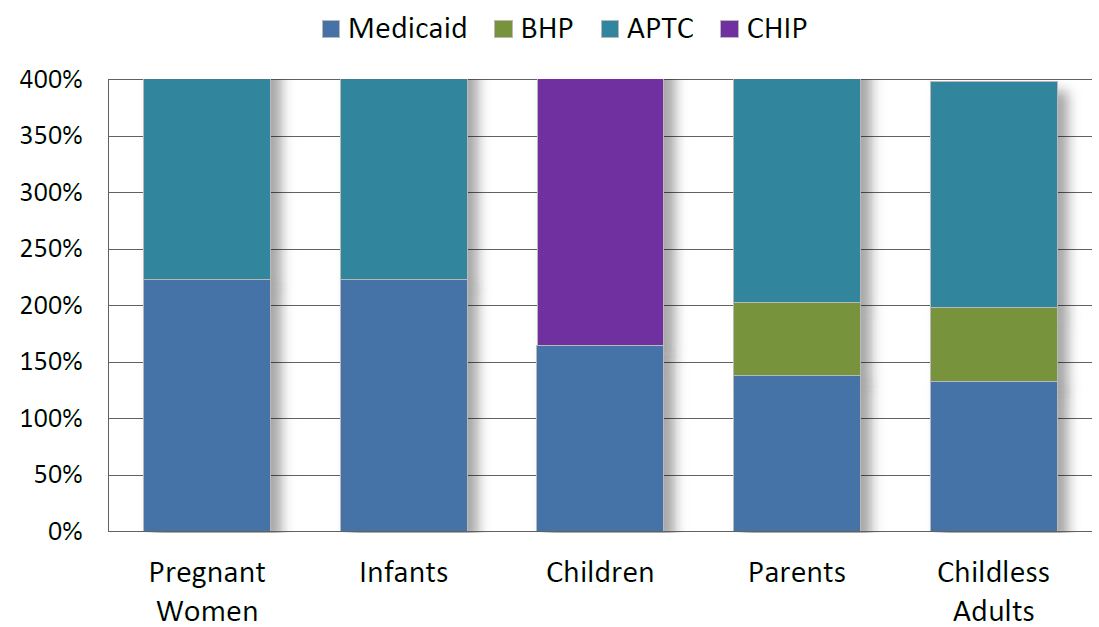

How BHP Fits Into Health Coverage Eligibility Levels

Who is Eligible for BHP?

- To be eligible for coverage under the BHP, individuals must meet the following requirements:

- Below age 65 at the beginning of the plan year;

- Resident of the State;

- Not eligible for Medicaid or CHIP;

- Not eligible for affordable minimum essential coverage;

- Income between 133% FPL – 200% FPL or < 133% and ineligible for Medicaid due to immigration status; and

- Individuals eligible for BHP are ineligible for Marketplace coverage.

Potential Advantages and Disadvantages of a BHP in NY

- Potential Advantages

- State cost savings

- Greater consumer affordability

- Reduction in uninsured

- Reduction in provider bad debt

- Potential Disadvantages

- Impact on the size of the Marketplace

- Impact on premiums in the Marketplace

- Increase in uninsured

Decisions Needed From CMS

Financing

- How will BHP financing work?

- How will CMS calculate the value of APTC and cost sharing subsidies that would have been provided to the individual in the Marketplace?

- How will CMS implement annual reconciliation?

- Will states be given 100% of the value of cost sharing reductions?

- Will CMS permit states to use 90% FMAP to fund IT System modifications to implement a BHP?

Impact on Marketplace

- Will CMS allow states to pool risk between BHP and the Marketplace?

- Will CMS require the BHP to mirror Medicaid rules or Marketplace rules or give states flexibility to decide?

Eligibility and Enrollment

- Whether to have open or rolling enrollment?

- Whether eligibility rules always follow tax filer rules or whether non–filer rules can apply in special exceptions?

- Will CMS permit states to provide 12–month continuous coverage for BHP enrollees?

Other Logistics

- Rules around notices and administrative hearings.

- Network adequacy rules.

- Essential community providers.

- Health plan accreditation.

State Decisions

Financing and Administration

- Does the Federal financing for the BHP fully fund the program with no new state dollars?

- Is the funding sustainable?

- What is the value of potential state savings?

- How will program administration be funded?

- How will QHP enrollees be transitioned if BHP is adopted?

Cost–Sharing

- What level of cost–sharing should BHP adopt?

- Premium contributions.

- Co–payments to providers.

- An individual in Medicaid at 138% of FPL pays no premiums.

- An individual in a QHP at 180% of FPL ($20,700) pays about $90 a month in premiums.

Benefits and Health Plan Selection

- The Benefit package must be at least the Standard Silver Essential Health Benefit.

- Does the State want to add any benefits?

- How will BHP plans be selected?

Provider Reimbursement Rates

- Should provider reimbursement rates be set at Medicaid rates, Medicaid plus, or Commercial rates?

- Will the funding levels support higher rates than Medicaid?

Impact on NYS: Studies to Date

Open Discussion/Comments

Next Steps

- Next Meeting

- September 9 or October 8 from 10 AM – 1 PM.

- Meeting Date dependent on CMS regulations.

- New York City, NYS Department of Health Metropolitan Area Regional Office 90 Church Street, 4th Floor, Conference Room A/B, Manhattan.

- Questions? Please contact: Kalin Scott, kid01@health.state.ny.us or (518) 474–8141

Follow Us